Attorney and guardian Mary Rowan

Rowan kidnaps partly-blind young woman without notice to her mother, who has co-guardianship, or court order

Places her in unlicensed group home with other Rowan wards

Residents of home pay $600 rent to share one bedroom, out of SSI checks

Put on close-to-starvation diet, subjected to bedbugs, abuse

Ward petitions Judge Judy Hartsfield to remove Rowan

By Diane Bukowski

August 28, 2017

Rowan assistant Katie McDonald

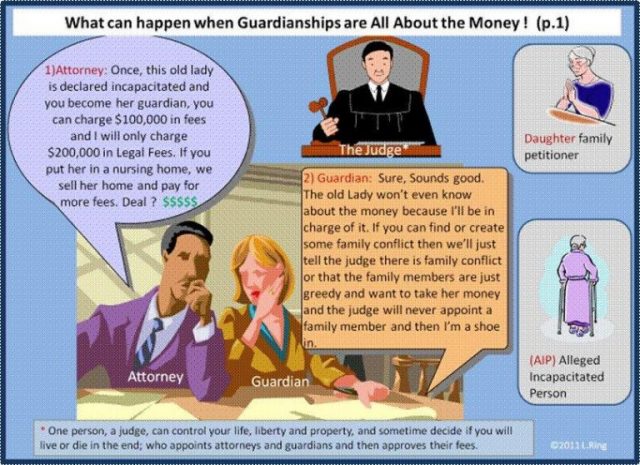

VOD Editor: This is one of a series of stories VOD has done on what amounts to vicious abuse by guardian and attorney Mary Rowan. Her usual M.O. is to wrangle guardianship papers from the many Wayne County Probate Court judges who appoint her, then immediately proceed to seize the ward from their current residence, without a court order of removal, without notice, and without bringing their clothing and personal belongings. She and her assistant Katie McDonald then place them in various venues including group homes without notifying their family members of their location.

The next step is to get control of the ward’s finances, and frequently move on to seize real and personal property. Perfectly competent, independent elders such as Gayle Robinson have been seized from their well-tended homes and eventually forced into nursing homes.

U.S.M.C. veteran Gayle Robinson with photo of her late husband Russell, also a veteran.

Today, according to her son Randy Robinson, Wayne County Probate Court Judge Terrance Keith heard arguments on removing Rowan as guardian and possibly placing Robinson with her daughter Kathy, in order to remove her from a nursing home with ties to Rowan allies. The entire family must agree to this arrangement. The next hearing on the matter is October 12.

Even under her daughter’s guardianship, Robinson would lose her independence and may lose her home of many years, where she raised her 10 children with her husband, both of them veterans. While held captive in the nursing home Rowan put her in, Mrs. Robinson was drugged and thoroughly traumatized.

During the hearing, Keith first threatened another son, Ricky Robinson, with arrest for kidnapping for bringing his mother to her own hearing from the nursing home. Rowan had forced her there with no court order from Keith. Rowan had forbidden many of Mrs. Robinson’s adult children from seeing or communicating with her.

At one point, Gayle Robinson fled the state to stay with her brother on the west coast, to avoid forced placement in a nursing home. Judge Keith jailed Randy Robinson indefinitely until his mother returned, although Keith had no jurisdiction over adults living in another state.

Sharmian Sowards with mom Wanda Worley before her current health crisis.

Meanwhile, Sharmian Sowards, a well-known country singer, has been battling charges brought by Mary Rowan against her in 33rd District Court, Brownstown Twp. The city has charged Sowards with “assaulting, resisting and obstructing” Rowan when she came to seize her mother Wanda Worley from her home.

Rowan had no court order of removal or showed Sowards any court papers at all. Sowards twice denied her entrance to her property. Worley is currently unable to leave her bed due to severe complications from spinal surgery and faulty pain management that followed. At one point she almost died, according to Sowards.

As her sole caregiver, Sowards said she cannot leave her mother’ s side and has asked 33rd District Court Judge Hesson for an adjournment of a trial set for Aug. 30-31, until her mother, her chief witness, recovers and the two can find transportation to the court hearing. The prosecution has complained that the next jury trial is not available until October, but Sowards says that is not a problem as long as her mother recovers.

Below is the petition filed by Kristina Brockington, 22, on Aug. 24 to remove Mary Rowan as her co-guardian, citing numerous violations of her rights as a ward and Rowan’s duties as a guardian. This is a move rarely used by wards because guardians do not inform them of their rights as they are required to do.

Below is the petition filed by Kristina Brockington, 22, on Aug. 24 to remove Mary Rowan as her co-guardian, citing numerous violations of her rights as a ward and Rowan’s duties as a guardian. This is a move rarely used by wards because guardians do not inform them of their rights as they are required to do.

Regina Gargos, Brockington’s mother, has started a Facebook page on Mary Rowan, titled “Victims of M*ry Rowan Wayne County Serial Kidnapper” at https://www.facebook.com/search/top/?q=victims%20of%20m*ry%20rowan%20wayne%20county%20serial%20kidnapper

Official declaration of Kristina M. Brockington, DOB 06/16/1995 Re: Wayne County Probate Court Case 2014-736670-GA (attachment to Terminate Guardianship of Mary Rowan Co- Guardian) to Wayne County Probate Judge Judy A. Hartsfield. Filed Aug. 24, 2017.

Wayne Co. Probate Court Judge Judy Hartsfeld

In keeping with MCL § 700.5310 (2)(3), and MCL § 700.5310 (a)(b) I Kristina M. Brockington, am petitioning Wayne County Probate Court to terminate Mary Rowan’s C0-Guradianship of myself, and to give, my mother and legal Co-Guardian full permanent guardianship of myself. Per state law, I am requesting a hearing on this matter as required within 28 days. My mother, Regina M. Gargus was originally appointed as my guardian by this court, to which I had no objection.

Mary Rowan was appointed as Co-Guardian by this court to assist my mother in helping me to secure housing, as this court had determined that my home was not suitable, which if I had been there, however; unable at that time due to an injury; I would have objected to that analysis.

During the term of her Co-Guardianship, Mary Rowan has grossly violated my rights as a ward and her duties as a guardian. She NEVER gave me a personal notice of her appointment, NEVER consulted me about major decisions affecting me, and has done nothing to secure services for me, so that I can return to managing my own affairs, as my mother has.

She has not made adequate provisions for my care, comfort and maintenance. Instead:

Took me from my home in Livonia where I was living with four other girls that were of my peer. She informed us through her aide Katie McDonald, that I did not have a choice.

Kristina Brockington, 22, back with her mother who nursed her back to health but was threatened by Mary Rowan for removing her from bedbug-infested group home.

She put me in a group home that was a 2 br. Brick home in Detroit, and was 40 minutes from not only my mother, but all of my friends and family. I felt extremely alone and isolated. I went from being around my friends, family and mother on regular bases, to being completely isolated, as no one was nearby. My mother could not help as much as before, due to being that far away.

While I was in the group home, I was assaulted twice, threatened not only by a resident with serious mental issues on a daily bases, but at times the caregiver Andreana. Andreana would get in my face often and say things like “You know I can kick your ass?” These types of screaming threats were made at least once a week.

The caregivers, with the knowledge of the home provider, Lesa Judkins would offer me marijuana daily, even after this court asked me to stop, which they were informed. The last time I smoked with the caregiver Andreana was July 4, 2017.

My mother prior to Katie Mc Donald removing me without a court order, helped me to quit pot, and they were offering it to me; I partook, as I was depressed from being away from my hometown, family and friends. As long as I am in my mother’s care, she makes sure I do not use it, nor does she support it; and with her support I manage quit.

I was CONSTANTLY screamed at by the caregiver.

I was told by the caregivers and Lesa Judkins that we were NOT allowed to call 911 or call for an ambulance even if we feel we need to get medical attention. (this was made very clear, like a 10 commandment).

Kristina’s mother Regina Gargos

I was never allowed to go in the kitchen, even for a glass of water. We had to ask; and many times were denied, depending on the mood of the caregiver at the time. As you can imagine, this was VERY dehumanizing and humiliating as a completely competent adult; and one that is still trying to regain back her independence.

I was attacked twice by the same resident that suffered from severe Alzheimer’s disease, and was extremely aggressive; she would try to not only attack myself, but other residents and caregivers with forks and knives. The provider Lesa Judkins was informed more than several times that this resident is a threat not only to herself, but others. Lesa to this date has done nothing to resolve this issue. Katie Mc. Donald, the aide to Mary Rowan was also informed by me at our case management meeting.

The caregivers would make fun of me, sometimes jokingly, but not always. Made me feel insecure, and I would tell them that, but the teasing would continue.

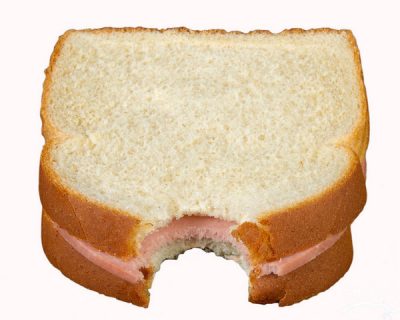

Bologna or ham sandwich for lunch every day, no vegetables

We ate the SAME THREE meals EVERYDAY! *Cereal * Bologna or ham sandwich* (Lunch was skipped at least 3 days a week, due to not enough for everyone}. Then dinner was a very small portion of over baked chicken and noodles stuff; never any vegetables, we never had any dairy. The only thing to drink was water or Kool-Aid. There was never a completely balanced meal, and most of the time there was never enough food.

The caregivers many times went into their own pocket to buy food. Sometimes it was due to not enough food; and other times, they were sick of the same three meal options as well. My mother would get me Jimmy Johns on the days there was not enough food. This would be the only times I would get anything fresh or fresh vegetables. Almost all of their condiments were outdated by up to three years.

When I got a new roommate, another Mary Rowan ward (4 out of the 8 people were ALL Mary Rowan Wards, and NONE of them never met her, which violates state guardianship law that guardians must see their wards every three months.) She came with no belongings. She was 50 and had the mind of a 10 year-old I would guess, and had a serious seizure disorder. She was there for 10 days with no clothes, hygiene products or anything. She and I made several calls to Katie McDonald with continued false promises. Katie Mc. Donald then left town to get married last I heard, at that time.

By day four, my roommate was not feeling well at all. She was not drinking, or eating, and her seizures were getting worse every day. I was becoming very concerned about her wellbeing. Lesa was informed, and had the House DR. come out. My roommate was requesting hospitalization, and was denied by Lesa Judkins and the DR.

By day 5, I had tried to contact the only number I had; Lesa’s she would let the calls go to voice mail.

By day 5, I had tried to contact the only number I had; Lesa’s she would let the calls go to voice mail.

By day 8 my roommate was begging for an ambulance. Even though I was told I better never call them, I did. At that time I was threatened by the caregiver, and Lesa Judkins that if the ambulance would take her to the hospital, I would be going with them.

The Home was infested with bed bugs, and I suffered from bites and sores because of them. All of my complaints were ignored for months. I still have extensive scarring from them.

Lesa Judkins tied up a puppy pit bull to the corner of the yard for at least a week. He was in the sun, in the 92 degree weather with no shelter or shade; he was also forced to stay tied up in a rain storm; he would cry all day and through the night at times. The puppy was on a chain 3-5 feet in length, and due to the shortness of the chain; was literally laying in his own urine and poop. After a week, I made a complaint to Lesa, again ignored; so I contacted animal control at which point I informed Lesa, and she removed the dog to an unknown location after that.

Scars from bedbug bites on Kristina.

I was again threatened by Lesa, that next time she would take my phone and I’ll never find it again if I pull that “shit” again. I replied with “that is animal abuse” she replied “no it’s not. What I find disturbing is the fact that she is completely obtuse to the fact that it is abuse, and running homes for people with even more disabilities than me.

They have 8 people in a 2 bedroom home, 3 men live in the basement with no separate entrance, and block windows. My mother told me, that was against all city fire codes, as she used to work for a fire department as a Paramedic. One lady is literally living on the back porch, where there is no heat.

This court ordered my mom and Mary Rowan to have a case Management meeting at the group home, Mary Rowan was a no show, instead it was her aid, Katie McDonald. My mother took notes. I was present as well; and your honor ordered that the Co-Guardian discuss social services for me. Instead 43 minutes Katie went on and on about SSI and SSD and how she could do a better job as payee than my mother. She further discussed ways she could get more money for me.

Which is good; but was not the purpose of the meeting. I was interested what they could do for me as far as education, and my goals and dreams and ways I can achieve that; which she touched on a little but only after 43 minutes of trying to convince my mother to hand over my SSI to them. I actually walked out of the meeting. No disrespect your Honor, but that was not the intent of the meeting.

Two weeks later my mother recanted her statement at the meeting and told Katie after much thought, she would not sign it over, and I agreed. Katie yelled at her, and threatened her; stating they were going to go to court and tell your Honor that my mother is not a responsible repayee, and state that there is missing paper work, and so on. Which are accusations, as Katie McDonald does not have any of my SSI paper work or information.

Lesa Judkins mug shot

After the home provider Lesa Judkins threatened me more than once, my mother did a background on her and found that Lesa has an extensive criminal history; with the latest known arrest to be in May of 2016 fleeing and eluding police. Lesa has mug shots and criminal complaints all over the internet for scams and fraudulent activities. I have attached that to this petition.

I do not believe Mary Rowan has my best interest, and here are my reasons why:

I never met her, spoke with her only in a court room on July 13th since she has been appointed.

She never showed up to the meeting that THIS court ordered to take place July 14, 2017 @ 2 PM.

She took me from a home I was content in, and put me in a home where I was abused physically and emotionally. Where I was not eating enough, where I was being bitten by bugs every day, where the caregivers and provider offering me pot. Where there are people literally piled on top of each other. Where I was FORCED to pay 600 dollars a month to SHARE a room; where I was, I was only paying 375 dollars for a room all to myself.

Mary Rowan put me in a home against my will, that has been unlicensed and uninspected and FORCED me to pay 600 dollars to a criminal, with serious past charges.

NOT once has she ever shown interest in me, getting to know me, visiting me, spending time with me. Talking with me about my interests and future.

Rowan is seated in darker blue in this photo taken just before she kidnapped Mailauni Williams (r) and held her for six months, not letting her mother Lennette Williams know where she was. Photo by the late Cornell Squires, VOD reporter. RIP.

She contacted the Bureau of Services for Blind behind our backs and told my counselor that she was now representing me, and I no longer was going to use their agency; which was a flat out LIE! I contacted them back three weeks later and now have things back in progress. Due to her doing that, I am almost a month behind than where I should be in this process.

The only interest that Mary Rowan and her aide have shown is to get my SSI. Or any other monies they think they can get.

Mary Rowan is also currently under investigation for failure to remove a ward in January of 2017 from an unsafe home that burned down, and as a result, that blind vet that was her ward; perished in that fire; THREE months after she was ordered to remove him.

Mary Rowan is also under suspicion and current scrutiny for elderly abuse, neglect, removing wards illegally without court orders, and financial exploitation.

Mary Rowan currently has multiple complaints pending against her currently. (also attached to this petition).

Mary Rowan currently has over 1400 wards. No one can take care of that many. She gets up to 1800 per year per ward, not including any other monies that she gets from estates, and insurance policies, pensions, and SSI or SSD. I feel she is only motivated by money, and not the interests of any of her wards, including myself.

Kristina recuperating after liberation from group home.

I would like to keep Regina Gargus as my permanent guardian, because she has my best interests and always has contrary to their accusations. Here are the reasons why:

I called and begged my mother to come get me from that group home, and she did. I was scared for my life at that point. I was so traumatized that I felt I was on an edge of a nervous breakdown. My mother got me out just in time; I couldn’t take any more of that place Mary Rowan forced me into.

My mother rescued me from that home, and continued to keep me away from them despite them calling her with threats to force me back there. She refused; she put me before herself, knowing that this court could rule against her.

When I was back in her care, she treated me for all my bed bug bites. (Which you can see pics on our phones).

I had lost 30LBS since May, and my mother spent an entire week nursing me back to health, preparing healthy fully balanced meals, and started me on a vitamin regimen right away.

My mother stopped payment on Lesa’s rent check for August, and I had to buy all new EVERYTHING. I left most of my belongings because of the bugs.

Blind student at Kalamazoo participates in technology project fair.

My mother still helps me with my shopping, transportation, and doctor’s apts. My mother has done all this for me for the past 5 years going on, and will not stop.

She has me enrolled with services for the blind, and soon I’ll be going to Kalamazoo to learn how to live being blind, and still be independent. Mary Rowan just wants to keep me in her homes, and collect my money. That is not what I want to do with my life, my mother and I know I can do so much more. My mother believes in me, Mary Rowan just sees me as another “ward.”

I am very afraid of Mary Rowan, and what she is capable of doing. I feel she could ruin my life, even more than she already has; especially after what my mother researched.

I am asking your Honor to set a hearing within the required time limits, and to issue an order removing Mary Rowan as Co-Guardian, and make my mother Regina Gargus as my permanent Guardian, as she is the one who truly has my best interest as listed.

Sincerely,(Signed)___________________________________________________

Kristina Brockington 8/24/2017

VOD: The Wayne Co. Probate Court website lists this petition as filed, and gives a date of Oct. 12 at 9 a.m. for a hearing. It is unclear at this point if the hearing has been moved up.

HTS UNDER MICHIGAN LAW RE: GUARDIANSHIP APPOINTMENTS:

Rights of an individual with a guardian:

http://voiceofdetroit.net/wp-content/uploads/Rights-of-individual-with-guardian.pdf

Powers and duties of a guardian:

http://voiceofdetroit.net/wp-content/uploads/Powers-and-duties-of-guardian-mcl-700-5314.pdf

Michigan Mental Health Code re: placement of wards with developmental disabilities

http://voiceofdetroit.net/wp-content/uploads/MICHIGAN-MENTAL-HEALTH-CODE-RE-PLACEMENT-OF-WARDS.pdf

Guardianship petitions: Summary under Michigan Law

http://voiceofdetroit.net/wp-content/uploads/Guardianship-petitions-Summary-under-Michigan-Law.pdf

RELATED STORIES:

END GUARDIAN ABUSE! SUPPORT WANDA WORLEY, SHARMIAN V. MARY ROWAN, THURS. MAY 25

http://voiceofdetroit.net/2017/04/05/mary-rowan-kidnaps-wards-from-homes-destroys-lives-fatally-late-moving-one-from-unsafe-place/

MARY ROWAN KIDNAPS AGAIN! SUPPORT SINGER SHARMIAN, CHARGED FOR PROTECTING MOM

http://voiceofdetroit.net/2015/08/02/wayne-co-probate-judge-terrance-keith-guardian-mary-rowan-force-vet-gayle-robinson-84-to-flee/

http://voiceofdetroit.net/2014/12/27/mary-rowan-denies-family-visits-to-dying-grandmother-now-co-guardian-in-robinson-case/

http://voiceofdetroit.net/2014/10/23/serial-kidnapper-atty-mary-rowan-takes-second-adult-ward-from-home-without-court-order/

http://voiceofdetroit.net/2014/10/24/rosa-parks-godchild-mailauni-williams-found-judge-george-guardian-rowan-removed-from-case/

http://voiceofdetroit.net/2014/11/25/home-for-the-holidays-mailauni-williams-back-with-mom-after-6-month-kidnapping/

http://voiceofdetroit.net/2014/07/21/amber-alert-rosa-parks-godchild-mailauni-williams-missing-judge-kathryn-george-loots-estate-bars-mortgage-payments-on-her-home/

http://voiceofdetroit.net/2014/06/16/shady-probate-judge-kathryn-george-jails-mom-seizes-daughter-and-estate

#FREEKRISTINABROCKINGTON, #FREEGAYLEROBINSON, #FREEWANDAWORLEY, #FREESHARMIAN, #JUSTICE4RAYMONDDAVIS, #JUSTICE4MAILAUNIWILLIAMS, #ENDGUARDIANABUSE, #JAILMARYROWANJOHNCAVATAIONOW

Warren Mayor Jim Fouts, who recently was the focus of a scandal arising from alleged tapes of him making racist remarks, also lives north of I-696 as well, at 28170 Louise Drive, Warren, MI 48092. Fouts has discouraged Bell from raising his current complaint with the Justice Department, and earlier from challenging the Warren City Code’s ban on anyone with a felony record running for office in the city.

Warren Mayor Jim Fouts, who recently was the focus of a scandal arising from alleged tapes of him making racist remarks, also lives north of I-696 as well, at 28170 Louise Drive, Warren, MI 48092. Fouts has discouraged Bell from raising his current complaint with the Justice Department, and earlier from challenging the Warren City Code’s ban on anyone with a felony record running for office in the city.

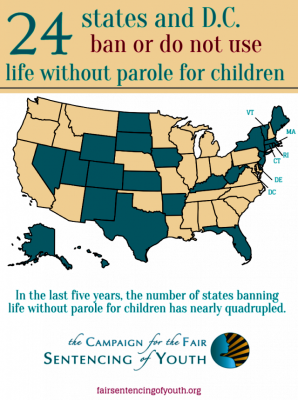

In 2012 the U.S. Supreme Court ruled that mandatory LWOP sentences for juvenile offenders are unconstitutional and ordered the resentencing of the nation’s 2,500 prisoners affected by the ruling. Prosecutors from several states ignored the landmark decision, including Michigan, claiming that it was not retroactive and did not apply to cases that had previously exhausted the direct appeal process.

In 2012 the U.S. Supreme Court ruled that mandatory LWOP sentences for juvenile offenders are unconstitutional and ordered the resentencing of the nation’s 2,500 prisoners affected by the ruling. Prosecutors from several states ignored the landmark decision, including Michigan, claiming that it was not retroactive and did not apply to cases that had previously exhausted the direct appeal process.

They specifically characterized Michigan and Louisiana as being among “a handful of extreme outliers that are flouting the [U.S. Supreme] Court’s dictate to limit JLWOP to the rare juvenile offender.”

They specifically characterized Michigan and Louisiana as being among “a handful of extreme outliers that are flouting the [U.S. Supreme] Court’s dictate to limit JLWOP to the rare juvenile offender.”

After I understood that this prosecutor’s language was an attack on my character, I began to bear witness to Hosea 4:6 which states, “My people are destroyed for a lack of knowledge.”

After I understood that this prosecutor’s language was an attack on my character, I began to bear witness to Hosea 4:6 which states, “My people are destroyed for a lack of knowledge.”